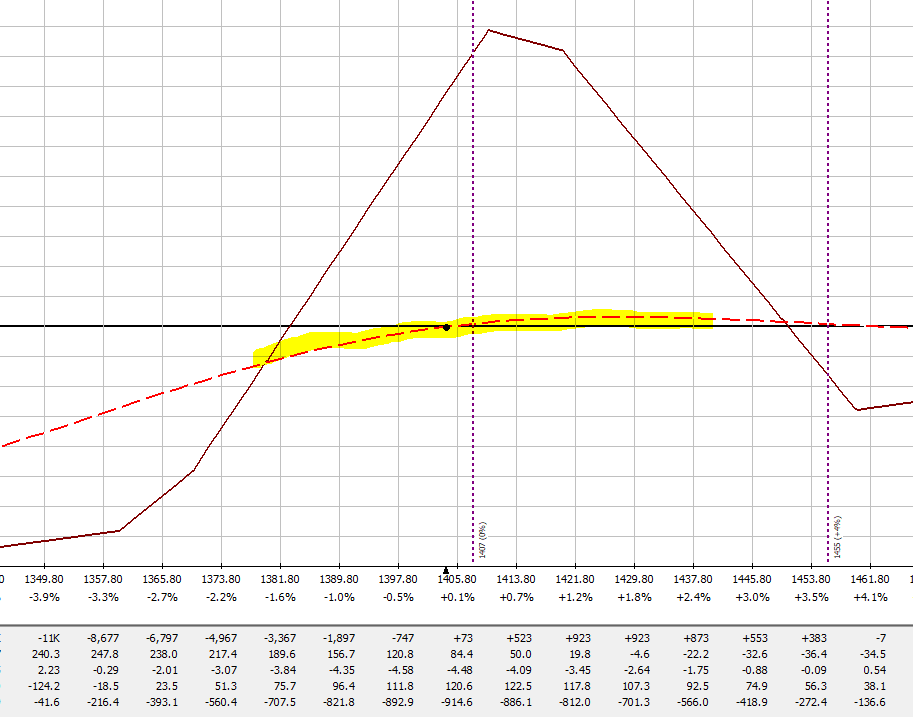

My Greeks look good, but my t+0 line to the upside is slightly sagging. Since the RUT has been down huge points in the past few days I think there will be a rally OR slight pullback to the upside. If looking at probabilities, the highest probability for the RUT to do is either pause or pullback (i.e. in this case pullback = upmove).

Considering all of this I should try and flatten out my t+0 to the upside.

Adjustment

Condor: Rolled 10 shorts up to 1340 and 10 longs up to 1290

Aug 23:

Self talk

My Greeks look good, should I try and flatten out my t+0 line to the upside more? WHY am I obsessing over this fucking line? STOP obsessing over the t+0 line.

Adjustment

Decided last minute to NOT make an adjustment.

Aug 30:

Self talk

My greeks are good, but my t+0 line to the upside is not flat. If I make an adjustment it ends up reducing my Delta e.g. starting delta -16 if I make an adjustment to flatten my t+0 my delta drops to -1.56. Should I be making an adjustment to flatten the t+0 to the upside?

Adjustment

I've decided not to make an adjustment and stay in the position the way it is.

Aug 31:

Self talk

Can't keep my VEGA and DELTA negative and RUT is 25 pts above my upper wing

Adjustment

Rolled the butterfly 30 pts up. I could not keep my 14 lot butterfly and therefore tried to keep my butterfly at 10 lot but due to capital requirements I was forces to buy a 9 lot butterfly.

Sept 6:

Self talk

I need to bring my put butterfly to at least a 10 lot, because that's what Dave said is the minimum number of bf's.

Adjustment

Added an additional 1 put butterfly to bring my M3 to a 10 lot.

Sept 7:

Self talk

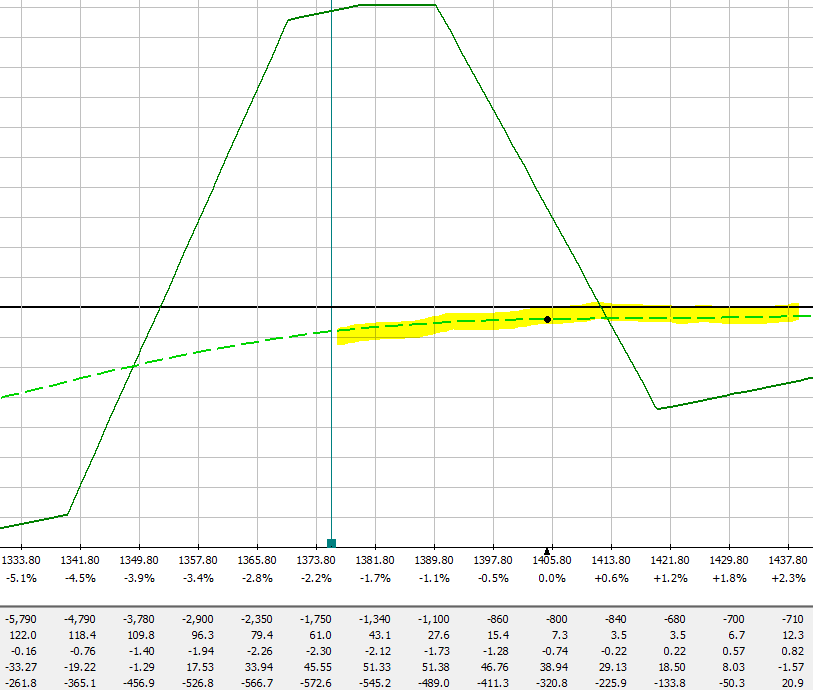

I need to balance my t+0 line out, I have too much risk to the upside. I should flatten the t+0 line to the upside.

Adjustment

I had to take money out of my deep ITM long call because I didn't have any cash in my account.

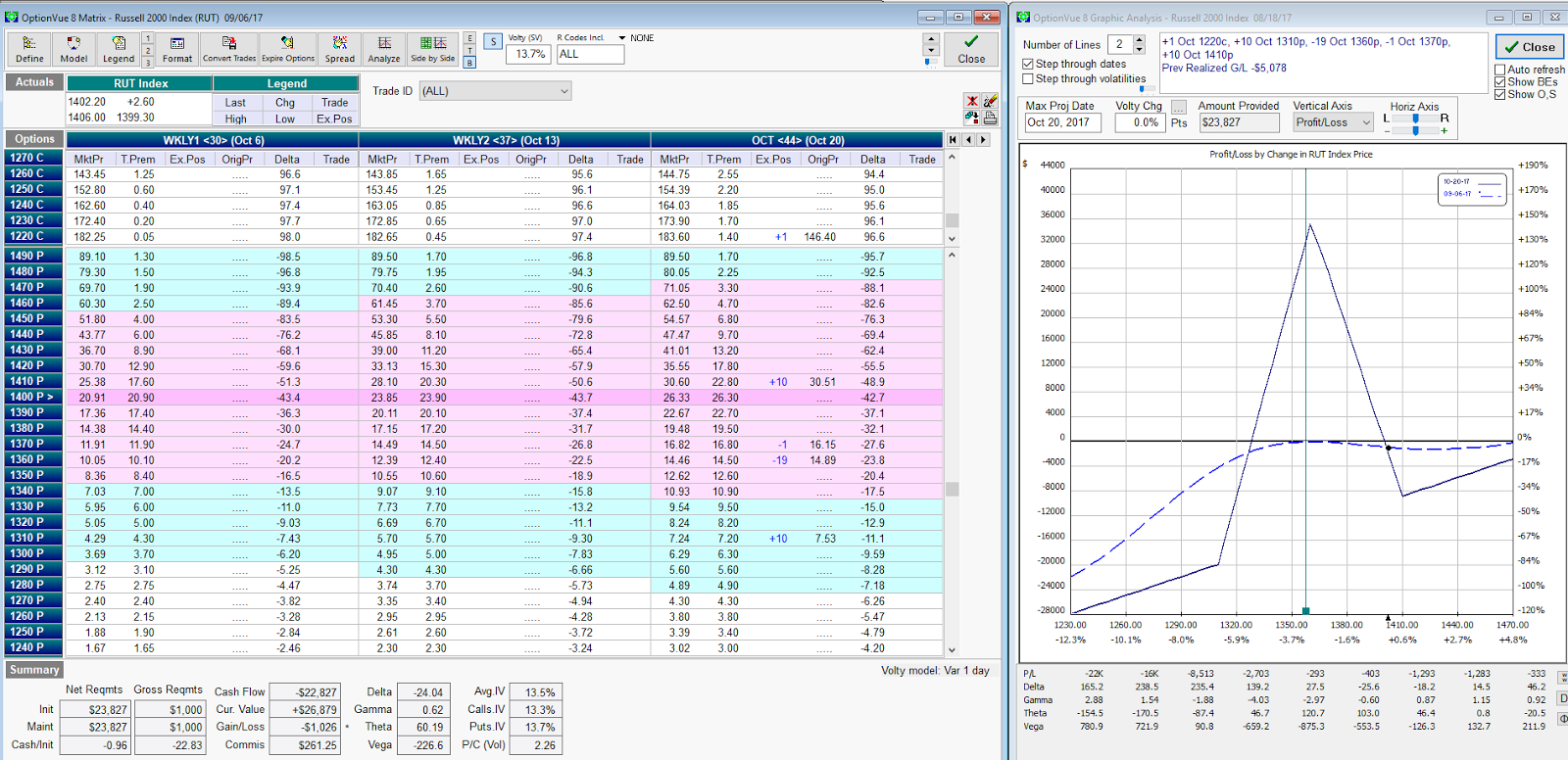

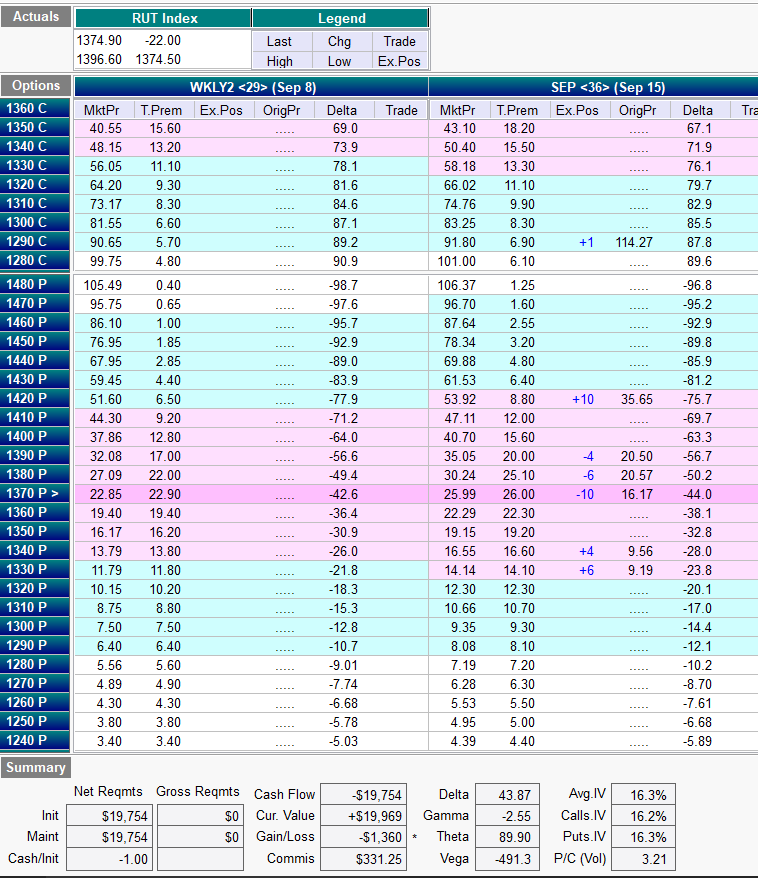

Diagonal trade from current month call to previous expiry Oct 13

Sold a vertical to balance t+0 to the upside

Sept 11:

Self talk

Maybe if I control Delta using a Call Vertical I won't have to make a drastic adjustment.

July 25 - Noticed that my t+0 to the upside was sagging a bit and a 30 pts move up would result in -$1042. Therefore I decided to adjust my position using a condor adjustment strategy.

Question: Should I have made this adjustment considering my Greeks were in check and it is so early in the trade?

After making the adjustment my upside with a 30 pts move -$774 AND 30 pts down move -$625

Jul 31 - Checked position DELTA & VEGA both are good. T+0 line is great also in 30 pts right/left.

I think that the market is going to rebound, b/c the market makers haven't taken all the value out of my position, contrarily I'm up in my position which is nice to see. What I think this is telling me is that the market makers believe that this dip is a slight pullback and the market will bounce.

Jul 31 - Concerned about my call and when to roll, I would have thought that with this down move that the calls would have become cheaper to roll, but that has not been the case.

Aug 1 - Checked position DELTA & VEGA and both are good. T+0 line is great in 30 pts right/left.

Concern about rolling my call, everything is still fairly expensive, will wait till Thursday to roll my call.

Trying to get within these rules:

Aug 2 - Checked position DELTA & VEGA and both are good (Delta was borderline for an adjustment 49.42). T+0 line is great in 30 pts right, but 30 pts to the left brings me to max loss.

20 pts move to the left (i.e. down) results in -$1250, which I'm ok with. Therefore making a judgement call based on the fact that on a large down move the highest probability for the RUT is there "might" be a rebound.

Aug 3- Position DELTA was not good (Delta = +80 Delta). T+0 line sloping down.

Decision: Roll M3 down 40 points, I was worried about doing this b/c I felt as I would be paying a premium to roll the position on a down day.

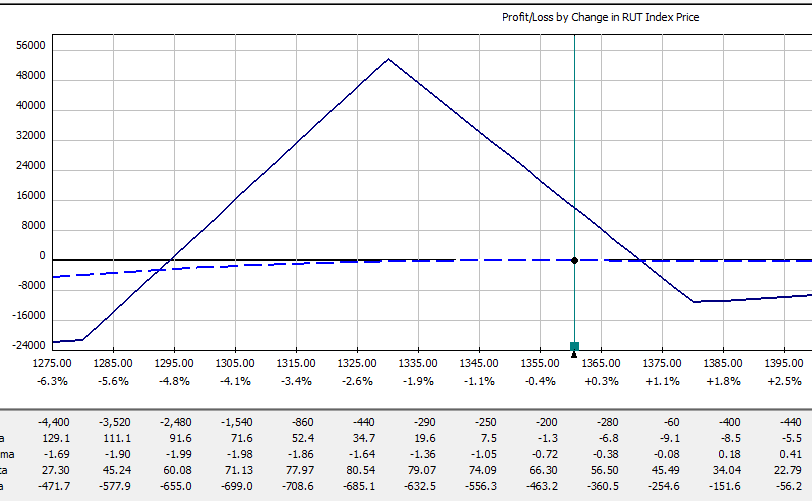

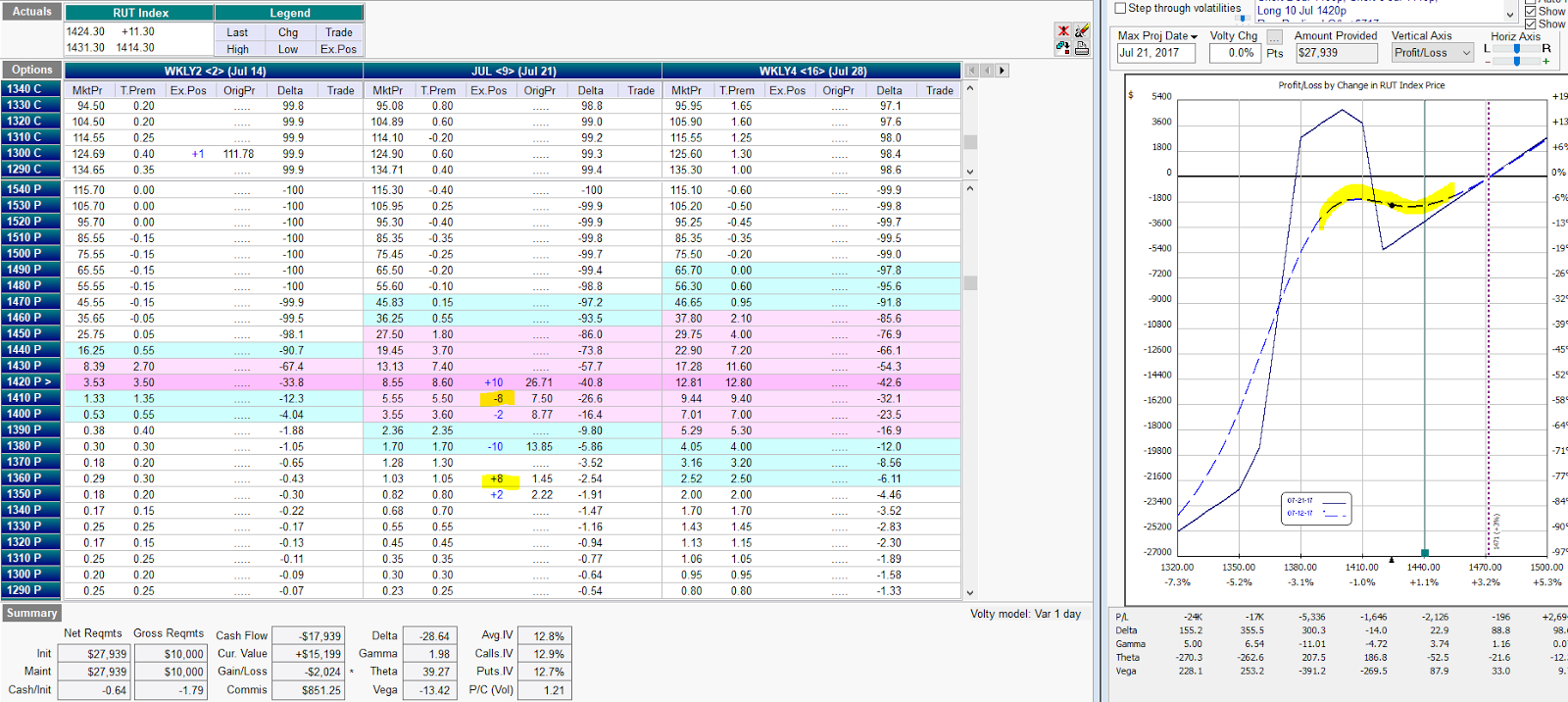

After rolling the M3 down 40 pts I moved half of my short strikes up into a +10 -10 -10 +10 M3 position, but when I look at my T+0 line 30 pts to the right (up) my t+0 was sagging

Therefore I ended up moving some more shorts up to maintain a "relatively" T+0 to the upside (i.e. right analyze graph) and protected 20 to 30 pts down (i.e. left of analyze graph 30 pts move = -$1554)

Question for Dave: How can I bring my position out from under the $0 axis?

If I add butterflies will that help bring my position above the $0 axis?

Aug 4 - The RUT bounced today position DELTA / VEGA was good (Delta = + 0.62 Delta). T+0 line was flat to the upside and 30 pts downside within -$1250 (actual greek trend -$1147).

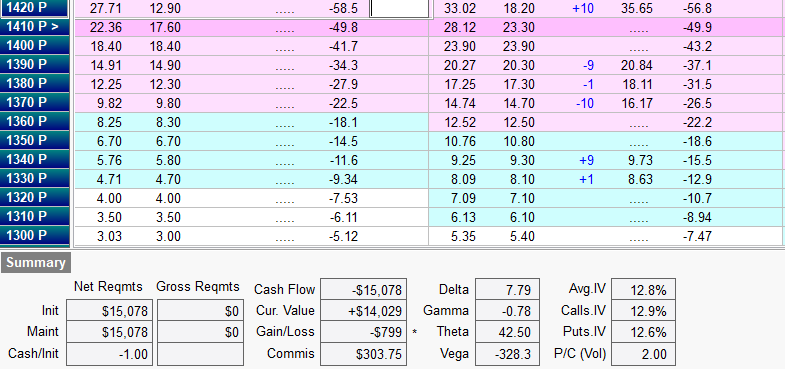

Decision: I found myself trying to increase my butterflies to take advantage of my Option Buying Power (I don't know how my M3 ended up being a $15,078 position size when every other time its closer to 18 or 20k) and an increase in volatility.

I couldn't figure out how to increase my position size without messing up my T+0 line.

Need to ask Dave or John how to achieve this.

Aug 7 - RUT was up 2.21 pts.

DELTA / VEGA are both good.

T+0 is relatively flat to upside and we are protected with a 30 pts down-move (-$750)

Aug 8 - RUT was up 0.46 pts.

DELTA / VEGA are both good.

T+0 is relatively flat to upside and we are protected with a 30 pts down-move (-$936)

Aug 9 - RUT dropped -16.80 points

10 am - Decided to roll my weekly call into the same expiry month as the butterfly, it was getting too complicated having to roll my weekly call. Hence, I decided to make my trade simpler for the time being and managing adjustments using Condors.

T+0 line: 30 pts down move will exceed -$2500 max loss

Ended up rolling using condor adjustment 5 from 1390 to 1380 and 5 from 1340 to 1330.

Aug 10 - RUT was down - 22 pts

Ended up rolling down 4 from 1390 to 1380 and 4 from 1340 to 1330

Aug 14 - RUT up +18.6 pts

T+0 line was sagging to the upside and therefore made an adjustment

Made adjustment using condor strategy, moved 10 x 1380 to 1390 and 10 x 1330 to 1340

Aug 17 - RUT was down - 20 pts and DELTA was +119.

Made an adjustment to sell 5 call verticals in order to control Delta, while the market is going bonkers.

I also moved using a condor strategy 10 x 1420 to 1410 AND -10 x 1370 to 1360

Had a conversation with Dave and he mentioned that if we have another down move that I should exit my position to limit my losses with the following steps:

Close call

Close condor

Close vertical

Aug 18 - BIG Mistake, at market open RUT was pulling back and I decided to exit the position. IF i had waited till noon or 3:30pm then I could have stayed in the trade and not lost as much money as I did.

*Entry Error*

When I put the M3 trade on, Dave said that my t+0 line was not ideal.

Adjustments:

May 17 - -34.30 point down move resulted in a +50 delta, per guidelines I had to roll my BF down. When I rolled down, I took some BF's off from my original 15 lot BF to 13 lot BF. Note: When I was live trading I remember that my Delta was above +50, but in back testing it shows as 48.

May 30 - Rolled my call forward AND Move 6 of my short strikes up to balance out my t+0 line (there was too much upside risk in my existing position)

June 2 - Vega went positive and rolled the entire position up + reduced my position to a 10 lot BF. Important - Ask Dave why did my position drop so much under the t+0 line? Was it b/c of a slight drop in volatility? OR the fact that I reduced my BF lot from 13 to 10 lot?

June 5 - Rolled call forward 1 month

MISTAKE: I don't know how it happened but I accidentally bought a 7 lot vertical on the bottom wing of my M3

June 6 - I reversed the mistake I made in the previous trading day of buying a 7 lot vertical spread AND rolled my M3 down 20 pts

I don't completely know why I did this - I think I made the adjustment b/c a 30 point drop would exceed my MAX loss of $2500 to the downside.

I should have just managed the position 20pts in either direction? Ask Dave.

Jun 13 - M3 went positive Vega and couldn't keep Delta and Vega negative concurrently therefore had to move the entire M3 up 20 pts

June 16 - Starting to see a ball on-top of a mound syndrome and made and adjustment to level out my risk on the t+0 line 20 to 30 pts in each direction.

June 19 - Greater than -50 delta outside tent and t+0 line sagging heavily to the upside. Pulled 4 lots from upper wing down to balance out the t+0 line

June 26 - Greater than - 50 Delta (actual -63.46) and therefore had to move some of my short strikes up. BUT I didn't have enough money in my account to make this adjustment therefore I moved some from the lower wing at the same time. Made the adjustment via an condor, this allowed me to make the adjustment with only having to pay for the cost of commissions.

I noticed after my adjustment that my Gain/Loss went down further WHY did this happen?

June 27 - Rolled my weekly call forward

June 30 - During live trading my position went above -50 Delta outside the tent AND there was an imbalance in the t+0 risk profile, therefore rolled 4 more up using the condor strategy and the lower wing.

July 5 - Delta outside tent breached -50 in live trading, therefore made an adjustment using a condor with 5 lots

July 6 - Large -18 point drop in the RUT caused my t+0 profile imbalance to the downside, therefore I made an adjustment to re-balance the t+0

Rolled my weekly call to the forward month.

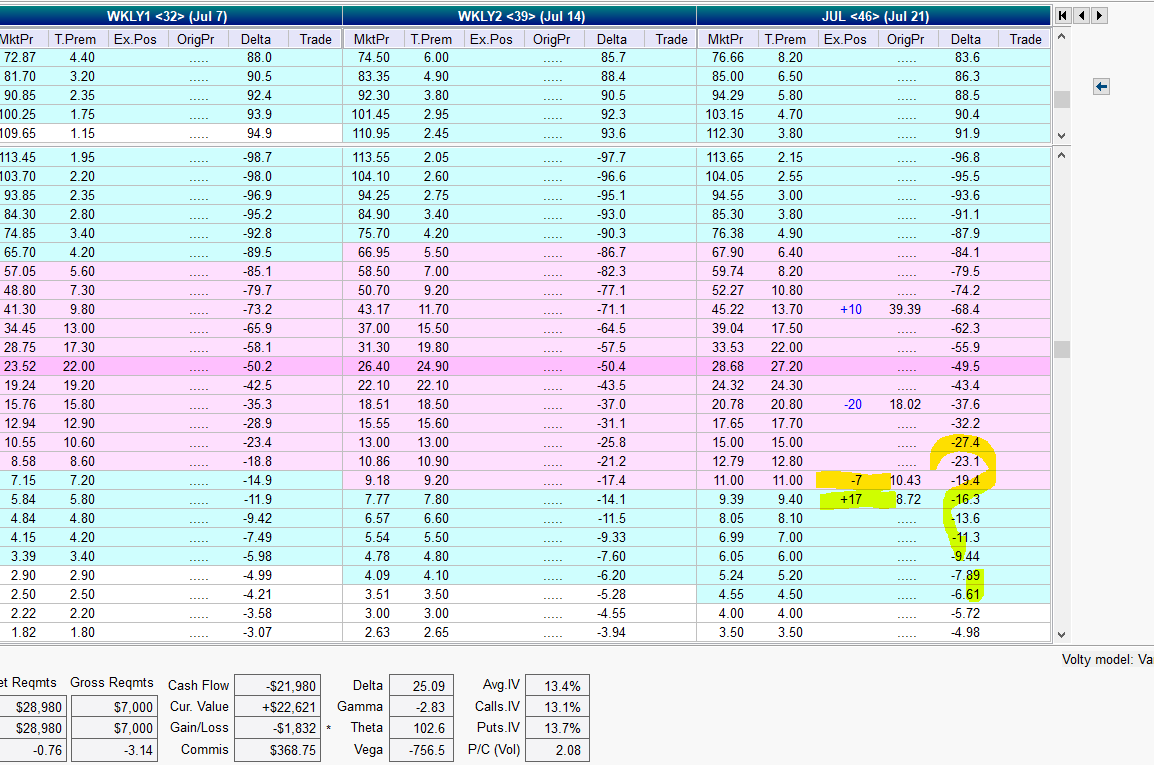

July 7 - Delta outside tent went to -95.85 and therefore moved 10 lot up using a condor strategy.

July 10 - the t+0 profile was imbalanced and there was too much upside risk, therefore I made an adjustment moving 2 lots up using a condor strategy

July 12 - Delta outside tent exceeded -50 (actually went to -86.20) and therefore moved another 6 lots up using condor strategy.

July 13 - Took the M3 off at max loss (-$2389.50 loss)

Summary:

I followed my rules and guidelines to a "T" and ended up in a shitty position.

Consulted Dave and he said that if I hadn't rolled down on the large -35pt drop in the RUT I would have been fine for the rest of my trade, which I find a bit difficult to swallow.

Made some adjustments along the way where I was reducing my M3 Lot size, I'm not sure if that had anything to do with my poor trade, but I'm going to backtrade this exact position an not reduce my BF size.

Another thing Dave mentioned was entry pricing and having the wind at your back. I get that BUT I don't 100% believe Dave's comment about not making an adjustment on the large down day.

I'll leave a summary of my backtesting in the comment section.